For new applicants, Puerto Rico remains undeniably superior to federal US tax rates, offering 100% tax exemption on interest, dividends, and capital gains for bona fide residents. The island's tax structure continues to attract luxury property investors seeking substantial savings on both capital gains and rental income.

Understanding these evolving regulations becomes critical for high-net-worth individuals considering Puerto Rico real estate investments.

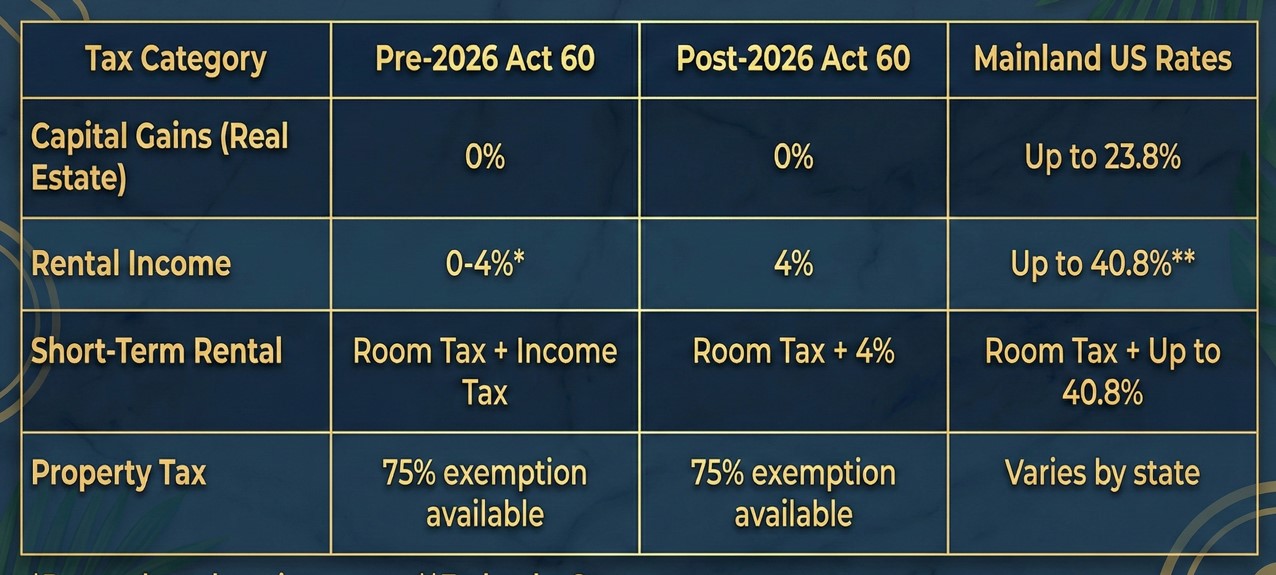

Key Takeaways

- Capital gains are 0% only on appreciation earned after you become a bona fide Puerto Rico resident.

- Appreciation earned before residency can still be taxed under U.S. federal rules.

- New Act 60 participants (from January 1, 2026) generally pay 4% on net rental income.

- Short-term rentals add Room Tax on top of income tax and require proper registration and collection.

Capital Gains Tax Rules for Real Estate Under Act 60

Real estate capital gains are treated preferentially under Act 60 incentives, maintaining the 0% tax rate that has attracted thousands of investors to the island. This benefit applies specifically to appreciation occurring after you establish bona fide residency in Puerto Rico. The key lies in timing your residency status correctly relative to your property acquisition or sale.

Capital gains from real estate differ fundamentally from gains on financial assets or business income. Property appreciation qualifies for a complete exemption when you meet all bona fide residency requirements and hold the asset after becoming a qualifying resident.

Bona Fide Residency Requirements for Real Estate Investors

Establishing bona fide residency demands more than simply purchasing luxury property in Puerto Rico. You must demonstrate genuine intent to make the island your primary home through multiple concrete actions. The IRS carefully scrutinizes these requirements, particularly for high-value real estate transactions.

Essential requirements include:

- Purchase or lease a qualifying residential property within two years of receiving your decree acceptance letter.

- Maintain physical presence in Puerto Rico for more than half the year (183+ days).

- Establish local banking relationships and conduct primary financial activities on the island.

- Make an annual $10,000 charitable contribution to qualifying local non-profit organizations ($5,000 to general non-profits and $5,000 to approved child poverty eradication funds).

- Obtaina Puerto Rico driver's license and voter registration.

- File Puerto Rico tax returns as a resident.

Pre-Residency vs Post-Residency Capital Gains

The timing of your capital gains matters significantly under Puerto Rico tax law. Gains accrued before establishing residency remain subject to your previous jurisdiction's tax rates, typically federal rates for US citizens. Only appreciation occurring after you become a bona fide resident qualifies for the 0% capital gains treatment.

- For U.S. citizens, pre-move appreciation may still face U.S. federal tax. Sourcing rules vary, so confirm how your property is treated before assuming a 0% rate.

This creates strategic opportunities for luxury property investors. You might consider establishing residency before major property improvements or during market upswings to maximize tax-free appreciation.

Rental Income Tax Obligations and New 2026 Rules

Rental income taxation underwent significant changes, including a rental exemption, with new Act 60 regulations taking effect January 1, 2026. Applicants who received their decree acceptance letter before this date maintain their original tax benefits. This includes potential exemptions on passive income.

- While bona fide residents benefit from 0% on interest and dividends, rental income is typically taxed as ordinary income unless the property qualifies as a tourism activity or under specific business incentives.

- The 4% tax on passive income applies to all rental income generated by new Act 60 participants.

This rate remains substantially lower than mainland US tax rates, which can reach 37% for high earners plus state taxes.

Short-Term Rental Tax Considerations

Short-term rental properties are subject to additional taxation beyond standard rental income rates under Puerto Rico's Room Tax system. This tax applies to accommodations rented for periods less than 30 days, similar to hotel occupancy taxes. Property owners operating luxury vacation rentals must register with the Puerto Rico Tourism Company and collect these taxes from guests.

Room Tax rates vary by municipality and property type:

- General Room Tax: 7% on gross rental income (applies to most short-term rentals island-wide).

- Dorado and Río Grande: 7% on gross rental income.

- Culebra and Vieques: 6% on gross rental income.

- Other municipalities: 5-8% depending on local ordinances.

Long-Term Rental Income Treatment

Long-term rental agreements exceeding 30 days avoid Room Tax obligations but remain subject to the new passive income tax structure. Property owners benefit from standard rental property deductions, including maintenance, property management fees, and depreciation. These deductions apply before calculating the 4% tax on net rental income for new Act 60 participants.

Existing Act 60 beneficiaries who obtained their decrees before 2026 may qualify for continued exemptions on rental income, depending on their specific decree terms and compliance history.

Comparing Tax Scenarios: Before and After 2026

The tax landscape shifted dramatically for new Act 60 applicants beginning in 2026, while existing beneficiaries retained their original terms. Recognizing these differences helps luxury property investors evaluate their optimal timing and strategy. The changes primarily affect passive income treatment rather than capital gains benefits.

A comprehensive comparison reveals the ongoing advantages of Puerto Rico residency even under the updated rules.

*Depending on decree terms and business structure

**Federal rates plus state taxes where applicable

IRS Section 933 and Federal Tax Implications

Section 933 covers only Puerto Rico-sourced income; U.S.-sourced income, including mainland services and some U.S. real property gains, may still face federal tax. This provision applies to both capital gains and rental income earned in Puerto Rico, preventing double taxation. The exemption requires maintaining proper documentation and filing requirements with both Puerto Rico and federal authorities.

Compliance with Section 933 demands careful record-keeping and professional tax preparation. You must demonstrate that income originates from Puerto Rico sources and meets all residency requirements.

Documentation Requirements

- Annual Puerto Rico tax returns filed as a resident.

- Federal Form 8898 (Statement for Individuals Who Begin or End Bona Fide Residence in a US Possession).

- Detailed records of days spent in Puerto Rico vs mainland US.

- Property ownership documentation and rental agreements.

- Bank statements showing Puerto Rico financial activity.

Potential Compliance Challenges

The IRS actively audits high-income taxpayers claiming Puerto Rico residency benefits, particularly those with substantial real estate holdings. Common audit triggers include insufficient time spent on the island, maintaining stronger ties to mainland locations, or inadequate documentation of residency intent. Professional guidance is essential for successfully navigating these requirements.

Working with experienced tax professionals familiar with Puerto Rico regulations helps ensure compliance and maximize available benefits.

Investment Timing and Property Criteria

Luxury property investors must balance Act 60 tax incentives with core real estate fundamentals. Prime coastal enclaves like Dorado, Condado, and Palmas del Mar deliver the strongest combination of tax savings, lifestyle amenities, and durable rental demand.

Strategic Acquisition and Residency

Timing remains critical under evolving regulations. Establishing bona fide residency prior to major property improvements or market upswings captures the maximum benefit from preferential capital gains treatment on future appreciation. Tax benefits should always complement, rather than drive, the underlying investment strategy.

Key Selection Factors:

- Dual Utility: Target assets that satisfy Act 60 residency requirements while generating consistent rental income.

- Market Fundamentals: Prioritize locations with proven appreciation, reliable infrastructure, and premium tenant demand.

- Professional Alignment: Coordinate property selection with tax counsel to refine the optimal timing for purchase and renovation.

While 2026 rule changes create urgency regarding passive income treatment, Puerto Rico maintains a distinct advantage over mainland U.S. tax regimes. Qualified buyers who document genuine ties to the island continue to realize significant long-term value through disciplined property selection.

Puerto Rico Luxury Properties for Sale

Christie's International Real Estate Puerto Rico specializes in connecting discerning investors with exceptional luxury properties for sale that meet both Act 60 requirements and investment objectives. Our portfolio includes prime beachfront estates, historic Old San Juan residences, and modern luxury developments across the island's most sought-after locations.

2200 DORADO BEACH DR #3 DORADO PR, 00646

This iconic East Beach, Ritz-Carlton Reserve–branded estate offers ultra-private, resort-style living on a lush acre with expansive indoor-outdoor entertaining, a showpiece kitchen, spa amenities (sauna, cold plunge, outdoor bathing), and a serene pool setting moments from Dorado Beach Resort and Spa Botanico.

9 CASTAÑA ST GUAYNABO PR, 00968

9 Castaña St. is a rare 1.2-acre multigenerational estate in San Patricio, offering over 10,000 square feet of refined living, 7 bedrooms, resort-style outdoor amenities, expansive entertaining spaces, backup power and water systems, and convenient access to Condado and Dorado.

5R MOUNT RESACA BARRIO FLAMENCO, CULEBRA, PR 00775

Hilltop Vacation Rental Homes is a 5-building Culebra investment property on Mount Resaca with panoramic Caribbean views, five rental units, pools, solar and water systems, strong rental history, and close access to beaches, town, the airport, and ferry dock.

10 RIDGETOP HUMACAO PR, 00791

Perched above Palmas del Mar, this historic Charles Fraser-built estate offers sweeping ocean, mountain, and resort views, elegant Mediterranean-inspired interiors, expansive terraces, a poolside outdoor kitchen, and rare access to one of Puerto Rico’s most prestigious coastal communities.

Final Thoughts

Even with the 2026 rule changes for new Act 60 applicants, Puerto Rico continues to offer compelling advantages for luxury property investors who plan carefully. Qualifying post-residency appreciation still enjoys 0% capital gains tax. This, combined with competitive rental income treatment, keeps the island attractive compared to high-tax U.S. jurisdictions.

At Christie’s International Real Estate Puerto Rico, we help you buy, sell, or rent luxury properties with clarity around location, lifestyle, and investment strategy—so you move with confidence. Explore our curated portfolio and speak with our team to match the right property to your goals. Reach out today and let us guide your next Puerto Rico real estate move from first viewing to final closing.

FAQs

Does Act 60 change how depreciation, repairs, and management fees affect my rental tax?

Yes. Rental income is generally taxed on net profit after allowable expenses (e.g., depreciation, repairs, insurance, property management, utilities you pay), so clean bookkeeping and properly categorized deductions can materially reduce the amount subject to the 4% rate.

If I rent my “primary residence” part of the year, can that create residency or compliance issues?

Potentially. Renting out the home you claim as your primary residence—especially for extended periods—can raise questions about where you truly live and whether your Puerto Rico home is available for your personal use, so structure and documentation matter.

What happens if I receive my decree but don’t buy a qualifying home within the required window?

You risk falling out of compliance with your decree conditions, which can jeopardize incentives and expose you to back taxes, penalties, or the loss of benefits. If timing is tight, discuss extensions or alternatives with Puerto Rico counsel immediately.

.png)