Financing a luxury home in Puerto Rico is absolutely viable, though it operates under distinct conditions from mainland U.S. markets. The key constraints include limited U.S. lender participation and higher down payment requirements, typically ranging from 20% to 30% for luxury properties.

This comprehensive guide covers the full lender landscape, loan structures, and qualification benchmarks to help you secure financing for luxury properties in Puerto Rico.

Key Takeaways

- Local banks lead luxury financing in Puerto Rico.

- Jumbo loans require more cash, credit, and reserves.

- Mainland lenders have limited Puerto Rico reach.

- Longer closing timelines demand early preparation.

- Ultra-luxury deals often need alternative financing.

Local Banks Dominate Puerto Rico Luxury Lending

.png)

Image Source: newsismybusiness wikipedia santarosamallpr

Financing for Puerto Rico luxury properties often centers around local financial institutions that understand the island’s unique market dynamics and regulatory environment. These banks maintain stronger relationships with high-net-worth clients and offer more personalized underwriting approaches than their mainland counterparts. The local banking sector includes institutions like:

- Banco Popular

- FirstBank Puerto Rico, and

- Oriental Bank,

These banks collectively handle the majority of luxury property transactions.

Local banks provide several advantages for luxury home buyers, including bilingual service teams and familiarity with complex property titles common in Puerto Rico. They also maintain more flexible debt-to-income ratios for qualified borrowers, particularly those with significant assets or investment income.

Documentation Requirements for Local Bank Financing

Local mortgage lenders Puerto Rico require comprehensive financial documentation that extends beyond typical mainland requirements. Borrowers must provide tax returns for the previous two years, bank statements covering six months, and detailed asset verification including investment portfolios and retirement accounts. Additional documentation includes employment verification letters, corporate financial statements for business owners, and proof of any rental income from investment properties.

The verification process also includes credit checks from both mainland and Puerto Rico credit bureaus when applicable.

- Federal and Puerto Rico tax returns (2 years).

- Bank statements from all accounts (6 months).

- Investment account statements and portfolio valuations.

- Employment verification or business financial statements.

- Property insurance quotes and flood zone determinations.

- Title search and property survey reports.

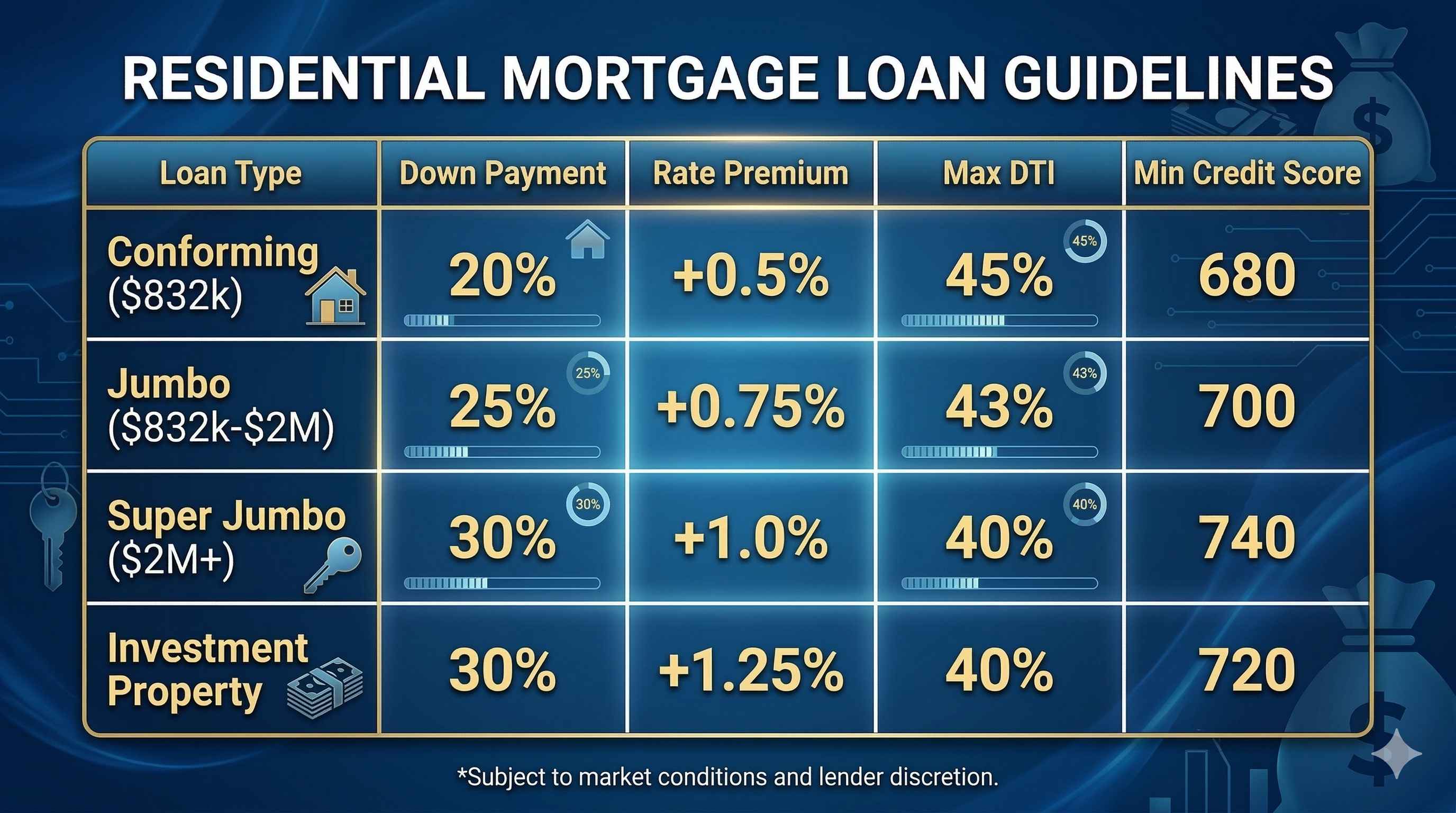

Jumbo Loan Thresholds and What They Mean for Your Budget

Jumbo loan Puerto Rico limits follow federal guidelines but application varies significantly among local lenders. The current baseline conforming loan limit for Puerto Rico stands at $832,750 for 2026, meaning any mortgage above this amount requires jumbo loan processing. Luxury properties in prime locations like Condado beachfront or Dorado Golf Resort typically exceed these thresholds, requiring specialized financing approaches.

- Down payment luxury home Puerto Rico requirements increase substantially for jumbo loans, with most lenders requiring 25-30% down payments for loans exceeding $1 million.

- Interest rates on jumbo loans also carry premiums of 0.25-0.75% above conforming loan rates.

Jumbo Loan Qualification Standards

Jumbo loan qualification involves stricter income verification and asset requirements compared to conforming loans.

- Lenders typically require debt-to-income ratios below 43% and cash reserves equivalent to 2-6 months of mortgage payments.

- Credit score requirements generally start at 700, with the best rates reserved for borrowers above 740.

- Asset verification becomes particularly important for jumbo loans, with lenders scrutinizing the source of down payment funds and ongoing income stability.

Interest Rate Structures for Luxury Properties

Interest rates for luxury property financing in Puerto Rico typically run 0.5-1.0% higher than comparable mainland rates. Fixed-rate mortgages dominate the luxury market, with 30-year terms being most common for primary residences. Investment properties carry additional rate premiums of 0.25-0.50%, reflecting the higher risk profile associated with non-owner-occupied properties.

Rate locks for luxury properties extend up to 90 days to accommodate longer closing timelines common in Puerto Rico transactions.

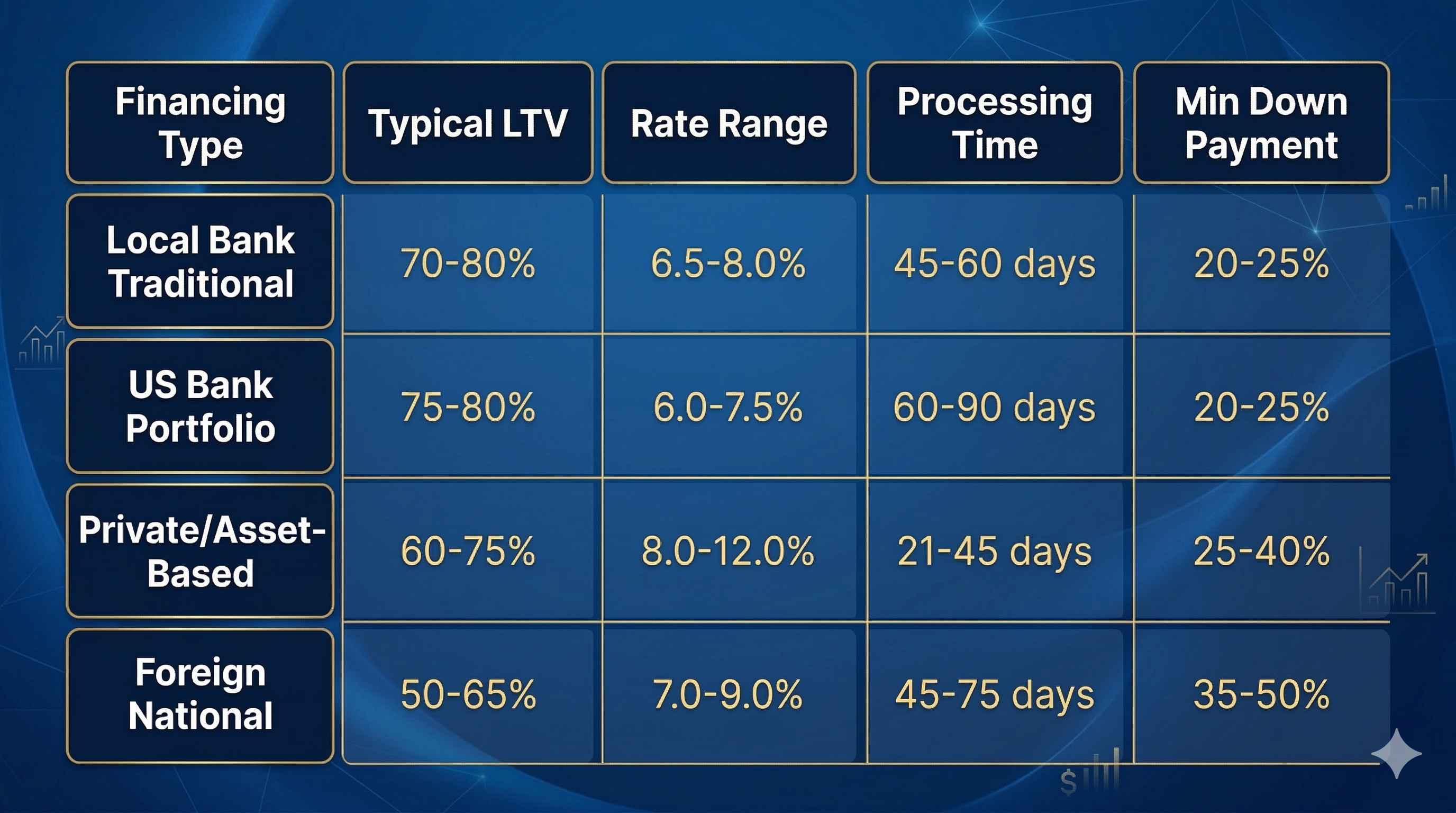

US Bank Mortgage Puerto Rico Property Access Points

Several mainland U.S. banks maintain limited Puerto Rico lending operations, primarily serving existing customers or those with substantial banking relationships. Mainland U.S. retail banks generally do not provide direct mortgage financing for Puerto Rico properties due to the island's distinct legal framework. These lenders typically focus on borrowers with established banking histories and substantial liquid assets.

Instead of using mainland retail banks, buyers must typically leverage existing mainland home equity or work with specialized private portfolio lenders and local Puerto Rico banks. The application process requires coordination between mainland underwriting teams and local Puerto Rico operations.

Mainland Lender Requirements

Mainland lenders impose additional requirements for Puerto Rico property financing, including mandatory property inspections by approved local appraisers and title insurance from companies licensed in Puerto Rico. Borrowers must also provide detailed explanations for their Puerto Rico property purchase, particularly for investment or second home transactions. Environmental assessments become more critical due to hurricane and flood risks.

Processing times with mainland lenders typically extend 60-90 days compared to 45-60 days with local banks.

Private Banking and Wealth Management Solutions

High-net-worth borrowers often access Puerto Rico luxury property financing through private banking divisions of major financial institutions. These programs offer portfolio lending solutions that consider total client relationships rather than individual loan metrics. Private banking loans can exceed traditional jumbo limits and offer more flexible terms for qualified borrowers.

Wealth management-based financing typically requires minimum investable assets of $1-5 million with the lending institution.

- Portfolio-based underwriting considering total client relationship.

- Flexible loan-to-value ratios up to 80% for qualified borrowers.

- Interest-only payment options for investment properties.

- Expedited processing through dedicated relationship managers.

- Cross-collateralization options for multiple property portfolios.

How to Navigate the 45-90 Day Closing Timeline

Puerto Rico luxury property closings require extended timelines due to comprehensive title searches, environmental assessments, and coordination between multiple parties including local attorneys, surveyors, and government agencies. The process typically spans 45-90 days from contract execution to closing, with luxury properties often requiring additional time for complex title issues or extensive due diligence. Buyers should plan financing applications to align with these extended timelines and maintain rate lock periods accordingly.

Successful navigation requires early engagement with local legal counsel and coordination between mainland and Puerto Rico-based service providers.

Critical Timeline Milestones

- Days 1-14: Financing application submission and initial underwriting review.

- Days 15-30: Property appraisal, survey, and environmental assessments.

- Days 31-45: Title search completion and insurance commitment.

- Days 46-60: Final underwriting approval and loan documentation preparation.

- Days 61-75: Attorney review and closing coordination.

- Days 76-90: Final walkthrough, funding, and deed recording.

Alternative Financing Strategies for Ultra-Luxury Properties

.png)

Ultra-luxury properties exceeding $3-5 million often require alternative financing approaches due to limited traditional lending options. Private lenders, family offices, and asset-based lending companies fill this gap by offering portfolio loans secured by multiple properties or substantial liquid assets. These financing solutions provide faster approval processes and more flexible terms but typically carry higher interest rates and shorter loan terms.

Foreign investors seeking luxury real estate often use private financing, offshore funds, or partnerships to structure their Puerto Rico property acquisitions.

Asset-Based Lending Solutions

Asset-based lenders focus on property value and borrower net worth rather than traditional income verification. These loans typically offer loan-to-value ratios of 60-75% with interest rates 2-4% above traditional mortgages. The approval process can complete within 30 days, making asset-based lending attractive for competitive luxury property purchases.

Borrowers must demonstrate substantial liquid assets, typically 1.5-2 times the loan amount, held in readily accessible accounts.

International Buyer Financing Options

International buyers face additional complexity in financing condo Puerto Rico and luxury home purchases due to limited credit history and income verification challenges. Specialized lenders offer foreign national programs requiring larger down payments (35-50%) but accommodate international income sources and credit profiles. These programs often require establishing U.S. banking relationships and providing extensive documentation of foreign income and assets.

Currency hedging becomes important for international buyers to manage exchange rate risk throughout the transaction process.

Puerto Rico Luxury Properties for Sale

Christie's International Real Estate Puerto Rico specializes in connecting discerning buyers with exceptional luxury properties for sale across the island's most prestigious locations. Our deep understanding of both local and international financing options ensures seamless transaction coordination for high-net-worth clients.

205 LUNA OLD SAN JUAN PR, 00901

This exquisite Old San Juan residence combines historic charm with modern luxury in the heart of the colonial district. The property features authentic architectural details and premium finishes throughout its carefully restored interior spaces.

40 LOS LAGOS DR PALMAS DEL MAR, HUMACAO PR, 00791

This pre-construction four-bedroom Model C home in Los Lagos offers 3,440 square feet, golf and lake views, refined interiors, and access to Palmas del Mar’s resort amenities.

CARR 1, KM 21.3 BO. LA MUDA GUAYNABO PR, 00969

This magnificent estate in prestigious Guaynabo showcases exceptional craftsmanship and expansive grounds with mountain views. The property features multiple entertaining areas, a resort-style pool, and meticulously landscaped gardens.

26 BARRIO PUNTAS SANDY BEACH RINCON PR, 00677

Situated on pristine Sandy Beach in Rincon, this luxury beachfront property offers direct ocean access and panoramic sunset views. The home features an open-concept design that maximizes the spectacular coastal setting and includes backup power systems.

Conclusion

Financing luxury properties in Puerto Rico requires strategic planning and understanding of the unique lending landscape dominated by local banks and specialized programs. Success depends on early preparation, comprehensive documentation, and working with experienced professionals who understand both local requirements and international buyer needs.

At Christie’s International Real Estate Puerto Rico, we help clients navigate the island’s luxury market with the local insight and strategic guidance needed to buy, sell, or rent exceptional properties. Whether you are exploring beachfront estates, historic residences, or investment opportunities, we work to make every step of the process more informed and more seamless. Contact us and let us help you find the right opportunity in the Puerto Rico luxury real estate market.

FAQs

Can I use a mainland U.S. pre-approval letter to make an offer in Puerto Rico?

Sometimes, but many sellers and listing agents prefer pre-approval from a Puerto Rico-based lender. This is because local institutions better reflect the island's unique underwriting, appraisal, and closing realities.

What property types can make financing harder for luxury buyers?

Homes with title irregularities, unpermitted additions, or unique construction can trigger tighter terms and larger down payments. You should review these items early in the due diligence process to avoid lender denial.

What should I budget for upfront cash beyond the down payment?

Plan for earnest money, appraisal costs, attorney fees, and insurance premiums like wind or flood coverage. These expenses and potential escrow reserves often total several additional percentage points of the purchase price.